The problem of private health insurance lies in its high costs and accessibility issues. Many individuals struggle to afford premiums and out-of-pocket expenses.

Private health insurance plays a crucial role in many healthcare systems worldwide. It provides coverage that often supplements public health services. However, rising premiums and complex policies create significant barriers for consumers. Many people find themselves underinsured or unable to afford necessary care.

This issue disproportionately affects low-income families and individuals with pre-existing conditions. As healthcare costs continue to climb, the need for reform becomes more pressing. Understanding the challenges of private health insurance is vital for consumers seeking effective solutions. Addressing these problems can lead to a more equitable and accessible healthcare system for everyone.

The Rise Of Private Health Insurance

The growth of private health insurance has changed healthcare. Many people seek better services and faster treatments. This shift affects costs, access, and quality of care.

Historical Context

Private health insurance has roots in the early 20th century. It began as a way to cover hospital costs. Here are key points in its history:

- 1930s: The first hospital insurance plans emerged.

- 1960s: Medicare and Medicaid provided public options.

- 1980s: Managed care organizations became popular.

- 2000s: Growth in employer-sponsored health plans.

These events shaped the landscape of healthcare. They paved the way for private insurance growth.

Current Market Dynamics

The private health insurance market is booming. Many factors drive this trend:

| Factor | Impact |

|---|---|

| Increased healthcare costs | More people buy insurance for financial protection. |

| Employer offerings | Employers provide insurance as a job benefit. |

| Technological advancements | Better treatments increase demand for coverage. |

| Regulatory changes | Policies encourage private insurance participation. |

Consumers now prefer private insurance for quicker access. They seek personalized care options. This shift raises questions about equity and affordability.

Credit: www.cambridge.org

Navigating The Coverage Maze

Private health insurance can be confusing. Many people struggle to understand their options. Choosing the right policy is essential for your health. The maze of coverage choices often feels overwhelming.

Policy Choices And Their Implications

Understanding policy choices is crucial. Different plans offer various benefits and costs. Here’s a quick overview:

| Policy Type | Benefits | Cost Implications |

|---|---|---|

| HMO | Lower premiums, limited network | Out-of-pocket expenses can be high for out-of-network care |

| PPO | Flexibility in choosing providers | Higher premiums, lower costs for in-network services |

| EPO | No referrals needed, lower cost | No coverage for out-of-network care |

Each policy type has unique features. Choosing the wrong plan can lead to unexpected costs. Know your health needs before selecting a plan.

Understanding Policy Limitations

Every policy has limitations. Understanding these helps avoid surprises later. Key limitations include:

- Coverage exclusions: Some treatments may not be covered.

- Waiting periods: Certain services may have delays.

- Annual limits: Some policies cap benefits yearly.

Always read the fine print. Look for hidden costs and exclusions. Ask questions if something is unclear.

Understanding these aspects helps navigate the coverage maze. Taking the time to research can save you money and stress. Choose wisely to protect your health and finances.

The High Cost Of Premiums

The cost of private health insurance premiums is rising. Many families struggle to pay these monthly fees. This affects their overall financial health. Understanding the reasons behind these costs is crucial.

Factors Influencing Premium Prices

Several factors determine health insurance premiums. Here are some key influences:

- Age: Older individuals usually pay higher premiums.

- Health status: Pre-existing conditions can increase costs.

- Location: Insurance costs vary by region.

- Plan type: Comprehensive plans often have higher premiums.

- Insurance company: Different providers set different rates.

The Impact On Household Budgets

High premiums significantly impact household budgets. Many families must adjust their spending. Here are some effects:

- Less money for groceries and basic needs.

- Increased stress and anxiety about finances.

- Delayed medical care due to high costs.

- Higher debt levels from medical expenses.

Many families feel the strain of rising premiums. The need for affordable healthcare is urgent.

| Household Item | Budget Impact |

|---|---|

| Groceries | Reduced spending on healthy food. |

| Utilities | Struggles to pay monthly bills. |

| Transportation | Fewer trips due to tight budgets. |

| Education | Less money for children’s activities. |

Understanding these impacts helps families make better financial choices. The high cost of premiums is more than just a number.

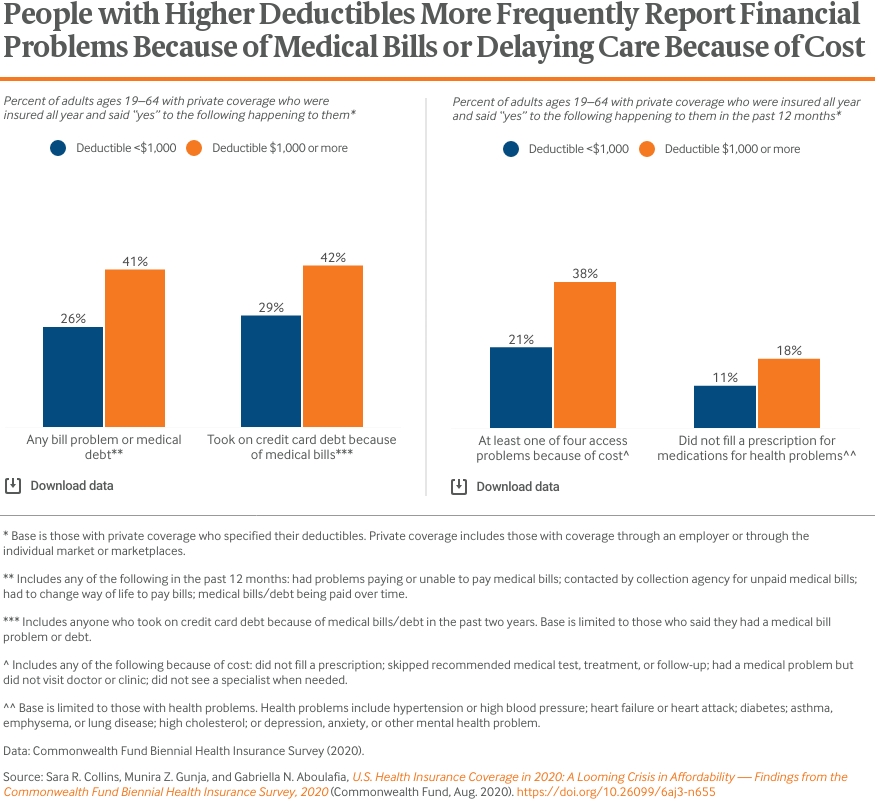

Deductibles And Out-of-pocket Dilemmas

Private health insurance often comes with complex terms. Understanding deductibles and out-of-pocket costs is crucial. These elements can cause significant stress for many patients. Let’s explore the impact of high deductibles and how patients cope.

The Financial Burden Of High Deductibles

High deductibles can create a heavy financial burden. Many people struggle to meet these costs. Here are some key points about this issue:

- High upfront costs: Patients pay a large amount before insurance kicks in.

- Delayed care: People may avoid necessary treatments due to cost.

- Debt accumulation: Medical bills can lead to overwhelming debt.

The table below shows average deductibles in the United States:

| Plan Type | Average Deductible |

|---|---|

| Employer-Sponsored Plan | $1,500 |

| Individual Plan | $4,000 |

| Family Plan | $8,000 |

Coping Strategies For Patients

Patients can use several strategies to manage high deductibles:

- Budgeting: Create a monthly budget for medical expenses.

- Health Savings Account (HSA): Save money tax-free for medical costs.

- Negotiate bills: Talk to providers about lowering costs.

- Payment plans: Set up a payment plan with healthcare providers.

- Preventive care: Use preventive services to avoid high costs later.

These strategies can help ease the financial burden. Understanding options allows better management of healthcare costs.

Pre-existing Conditions And Coverage Denial

Private health insurance often denies coverage for those with pre-existing conditions. This issue affects millions. Many people face difficulties accessing necessary medical care. Chronic illnesses add to their struggle. Understanding this problem is crucial for everyone.

The Struggle For Those With Chronic Illnesses

People with chronic illnesses experience significant challenges. They often face high medical costs. Insurance companies may refuse to cover treatment. This leads to:

- Increased financial burden

- Limited access to necessary medications

- Worsening health conditions

Many individuals feel helpless. They may avoid seeking help. This can lead to severe health complications. The emotional toll can be overwhelming.

Legislative Protections And Their Limits

Legislation has tried to protect patients with pre-existing conditions. The Affordable Care Act (ACA) is one example. It prohibits denying coverage based on health history. Despite these protections, gaps remain.

| Protection | Limitations |

|---|---|

| Cannot deny coverage based on pre-existing conditions | States can bypass some regulations |

| Essential health benefits coverage | Not all plans offer comprehensive coverage |

| Guaranteed issue rights | Some insurance companies still find loopholes |

Patients often navigate complex systems. They may face high premiums and out-of-pocket costs. The need for reform remains urgent. Addressing these issues can help ensure better health access for all.

Credit: www.commonwealthfund.org

The Underinsurance Issue

The problem of underinsurance affects many people today. Having health insurance does not always mean full coverage. Many people face financial strain due to gaps in their policies. Understanding underinsurance helps navigate these challenges.

When Having Insurance Is Not Enough

Many individuals believe they are fully protected by their health insurance. This belief can lead to unexpected costs. Here are some common scenarios:

- High deductibles increase out-of-pocket expenses.

- Limited coverage for specialist visits or treatments.

- Exclusions for certain pre-existing conditions.

- Insufficient coverage for prescription medications.

These gaps leave individuals vulnerable to high medical bills. Some may avoid necessary care due to cost concerns. This can worsen health conditions over time.

The Hidden Costs Of Underinsurance

Underinsurance comes with surprising hidden costs. Here are some financial impacts:

| Cost Type | Impact on Individuals |

|---|---|

| High deductibles | Forces upfront payments before coverage kicks in. |

| Out-of-network fees | Charges for seeking care outside the insurance network. |

| Limited annual limits | Caps on coverage leading to out-of-pocket costs. |

| Co-payments | Additional fees for each visit or treatment. |

These hidden costs can create financial burdens. Individuals may face tough choices about their health care. Understanding these costs is crucial for making informed decisions.

Access To Care: Inequality And Inefficiency

Access to care remains a major issue in private health insurance. Many people face barriers that prevent them from receiving timely and necessary medical services. Inequality and inefficiency in this system are significant challenges that affect millions.

Disparities In Healthcare Access

Healthcare access varies greatly among different groups. Factors like income, location, and insurance status create gaps. Here are some key disparities:

- Income level: Low-income individuals often struggle to afford premiums.

- Geographic location: Rural areas lack nearby healthcare facilities.

- Insurance status: Uninsured people have limited access to care.

These factors lead to unequal treatment and poorer health outcomes. The table below shows how different demographics experience healthcare access:

| Demographic | Access Level | Common Barriers |

|---|---|---|

| Low-Income Families | Low | High premiums, costs |

| Rural Residents | Moderate | Distance to providers |

| Uninsured Individuals | Very Low | Cost, lack of options |

The Efficiency Debate

Efficiency in healthcare is often questioned. Private insurance systems can lead to waste and duplication. Issues include:

- High administrative costs: Managing multiple plans adds complexity.

- Overlapping services: Patients may receive redundant treatments.

- Delayed care: Approval processes slow down access to necessary services.

These inefficiencies create frustration for patients and providers. Streamlining the system could improve access and care quality. Addressing these issues is critical for better health outcomes.

Credit: 44thand3rdbookseller.com

Policy Proposals And The Future Of Health Coverage

The debate around private health insurance is critical. Many proposals aim to improve health coverage. Understanding these proposals helps us envision a better future for everyone.

Evaluating Proposed Reforms

Many reforms have been proposed to address issues in private health insurance. Here are some key proposals:

- Universal Coverage: This aims to provide health insurance for everyone.

- Public Option: This allows people to choose a government plan.

- Cost Control Measures: These aim to lower health care costs.

- Increased Regulation: Stricter rules on insurance companies can enhance coverage.

Each proposal has strengths and weaknesses. A table below summarizes the main points:

| Proposal | Strengths | Weaknesses |

|---|---|---|

| Universal Coverage | Everyone gets health care. | High initial costs. |

| Public Option | More choices for consumers. | Could strain private insurers. |

| Cost Control | Lower expenses for patients. | Possible service reductions. |

| Increased Regulation | Better protections for consumers. | May limit company profits. |

Envisioning A Comprehensive Solution

A comprehensive solution must address many health care issues. Here are crucial aspects:

- Access: Everyone should have easy access to health care.

- Affordability: Health care must be affordable for all.

- Quality: Services should be high-quality and reliable.

- Transparency: Patients need clear information about costs.

Future health coverage must balance these aspects. Collaboration among government, insurers, and citizens is essential. A united effort can create effective health care solutions.

Frequently Asked Questions

What Are The Main Issues With Private Health Insurance?

Private health insurance often leads to high premiums and out-of-pocket costs. Many people face coverage gaps and limited access to certain services. Additionally, complex policies can confuse consumers, leaving them unaware of their benefits. These challenges can result in financial strain and inadequate healthcare for individuals.

How Does Private Health Insurance Affect Healthcare Access?

Private health insurance can limit access to care due to high costs. Many plans require significant copayments and deductibles. This can deter individuals from seeking necessary treatments. In some cases, providers may not accept certain insurance plans, further restricting patient options and leading to delayed care.

Are Private Health Insurance Plans Worth The Cost?

The value of private health insurance depends on individual needs. For some, it offers essential coverage and peace of mind. However, high premiums may not justify the benefits for others. It’s crucial to evaluate plan details and personal health requirements before making a decision.

Can Private Insurance Improve Health Outcomes?

Private insurance can improve health outcomes if it provides adequate coverage. Access to a wider range of providers and services enhances patient care. However, if affordability and accessibility are issues, the benefits may diminish. Ensuring comprehensive coverage is vital for better health outcomes.

Conclusion

Private health insurance poses significant challenges for many individuals. Rising costs and complicated policies often leave people confused and underserved. Understanding these issues is crucial for making informed decisions. Advocating for clearer options can lead to better health outcomes. It’s time to rethink how we approach health insurance for everyone’s benefit.

Leave a Comment